By

Growth, Inflation, and What Comes Next

As we move into the final quarter of the year, global markets have shown renewed strength. Investor optimism has been fueled by advances in artificial intelligence, expectations of interest rate cuts, and signs of resilience in the U.S. economy. But alongside this momentum, inflation remains persistent, and long-term yields are creating headwinds for certain sectors.

In this update, we take a closer look at what’s driving market performance, how economic indicators are shaping investor sentiment, and what it could mean for your financial strategy.

Global Markets Regain Momentum

Since mid-year, equity markets around the world have rallied. Global equity funds saw over $28 billion in net inflows in recent weeks, with U.S. funds leading the charge, followed by Europe and Asia. Bond funds also attracted capital, particularly in short-term and corporate segments.

This renewed energy has prompted some strategists to revise their forecasts. For example, BMO recently raised its year-end S&P 500 target to 7,000, citing stronger earnings and easing monetary policy. With the index currently around 6,650, that would represent a roughly 5% gain into year-end.

Still, investors remain cautious. Rising long-term Treasury yields could slow growth in capital-intensive sectors like technology and AI, even as enthusiasm for innovation continues to drive interest.

Regional Performance: A Closer Look

Developed markets posted solid gains in September, with Japan leading the way. Europe and the U.S. saw more measured advances. Global markets advanced 7.7%1 over the last 3 months and are up 18.9%2 year to date. The S&P 500 delivered an 8.1%3 total return for the quarter, bringing year-to-date gains to 12.4%4 for the year.

That said, the path hasn’t been smooth. Markets remain sensitive to inflation data, trade policy shifts, and global monetary trends. Volatility has persisted, but the broader direction has tilted upward.

U.S. Economy: Signs of Resilience

Recent data has added weight to a cautiously optimistic outlook. The final revision of second-quarter GDP showed annualized growth of 3.8% – a notable upgrade from earlier estimates. Stronger consumer spending, lower import drag, and resilient final sales all contributed to the upward revision.

Looking ahead, forecasts for full-year growth are centering around 1.9%, reflecting expectations for slower expansion in the coming months. Still, the data suggests that demand remains stronger than previously thought.

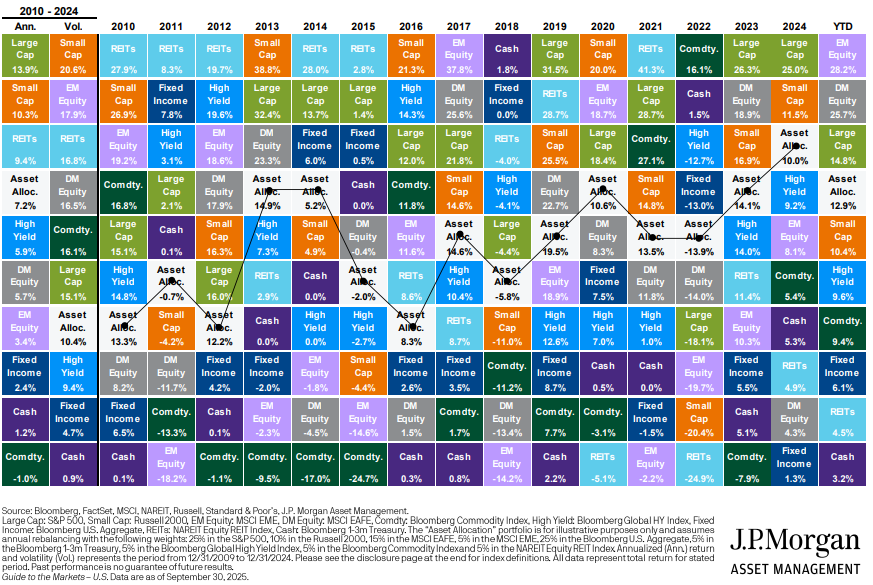

A Great Year for Diversification

Inflation and the Labor Market

Inflation continues to run hotter than many expected earlier in the year. The core PCE index (which excludes food and energy) held steady at 2.9% year-over-year in August. That persistence, especially in housing and services, indicates that underlying pressures haven’t yet eased decisively.

Meanwhile, the labor market is sending mixed signals. Job growth has cooled, and the unemployment rate has edged up. Weekly jobless claims recently dipped to 218,000, suggesting some resilience. Wage growth is also moderating, which adds complexity to the Fed’s balancing act between inflation and employment.

Credit Markets and Yield Behavior

The bond market reflects this uncertainty. The 10-year U.S. Treasury yield has moved higher following stronger GDP data, even after the Fed’s recent rate cut. Investors are pricing in both inflation risk and fiscal pressures. Credit spreads remain relatively contained, but volatility has increased as rate expectations shift.

Looking Forward: Positioning for What’s Next

The combination of stronger-than-expected growth and persistent inflation creates a delicate environment for investors. While upgraded GDP data offers room for optimism, inflation’s stickiness means that further rate cuts may be gradual and conditional – potentially limiting the tailwinds for equities.

In this environment, balance is key. Companies with long-term growth potential – particularly in AI, automation, and healthcare – remain attractive. At the same time, inflation-resilient sectors, high-quality bonds, and real assets can help absorb surprises. Diversification across geographies and asset classes continues to be a cornerstone of sound portfolio strategy.

Risk assets tend to perform well when fundamentals align and volatility subsides. But downside risks – from supply chain disruptions to policy missteps – should not be overlooked.

Hills Bank Perspective

At Hills Bank, our focus remains on helping clients navigate changing conditions with clarity and confidence. Our portfolios are positioned to capture opportunity while managing risk, and we continue to monitor developments in trade policy, geopolitical tensions, and broader economic trends.

If you’re thinking about how these shifts might affect your financial goals, we’re here to help. Your Wealth Management Officer can walk through your strategy and make sure it’s aligned with your long-term vision.

Some trust products and IRA contributions/balances are not a deposit, not FDIC insured by any federal government agency, not guaranteed by the bank and may go down in value.

[1] MSCI All Country World Index – Total Return, 6/30/2025 to 9/30/2025

2 MCSI All Country World Index – Total Return, 12/31/2024 to 9/30/2025

3 S&P 500 Index – Total Return, 6/30/2025 to 9/30/2025

4 S&P 500 Index – Total Return, 12/31/2024 to 9/30/2025